Many people don’t realize they can sell their life insurance policies for cash- often for much more than the surrender value. Managing personal finances during retirement can be a challenging and intimidating task, and staying on top of bills with limited income and resources requires intelligent planning. Life insurance premiums are a particularly burdensome cost that often increases with age, but you can help ease this stress by selling your policy.

Life insurance is a piece of property, much like your home, and you can sell it through a process known as a life settlement. In this transaction, the life insurance policyholder sells their policy to a third party. The third-party continue to make the monthly premium payments and ultimately collects the death benefit on the policy.

The policyholder benefits in two ways. First, they receive money immediately that can help pay for medical costs or any other expenses. Second, the policyholder no longer has to worry about premiums.

Your age, health status, policy type, and policy size all determine whether you are eligible for a life settlement. The older you are and the larger your policy, the more likely you will qualify. The amount you are paid for your policy also depends on certain factors. The insured’s life expectancy, future premium costs, and policy size all contribute to the final payout for the policy.

The Life Settlement Process

The process typically starts with the insured reaching out to their life insurance agent. The agent will recommend a broker to the policyholder. The broker then solicits bids to different life settlement providers (purchasers of life insurance policies) and identifies the best one. Brokers are obligated to work in the client’s best interest, but this assistance comes at a significant cost. Brokers and agents can take up to 30% commissions on the final payout, dramatically reducing the amount of money you earn for your policy.

Going directly to a provider presents its own benefits and challenges. Providers are trying to maximize their profits while making an offer you will accept. This essentially makes them a hostile party in a transaction. They want to pay you the smallest amount of money that you will agree to. Additionally, you will have to handle all of the paperwork and forms independently which can be confusing. While this avenue is more time-consuming and difficult for the policyholder, there are no broker’s fees or commissions.

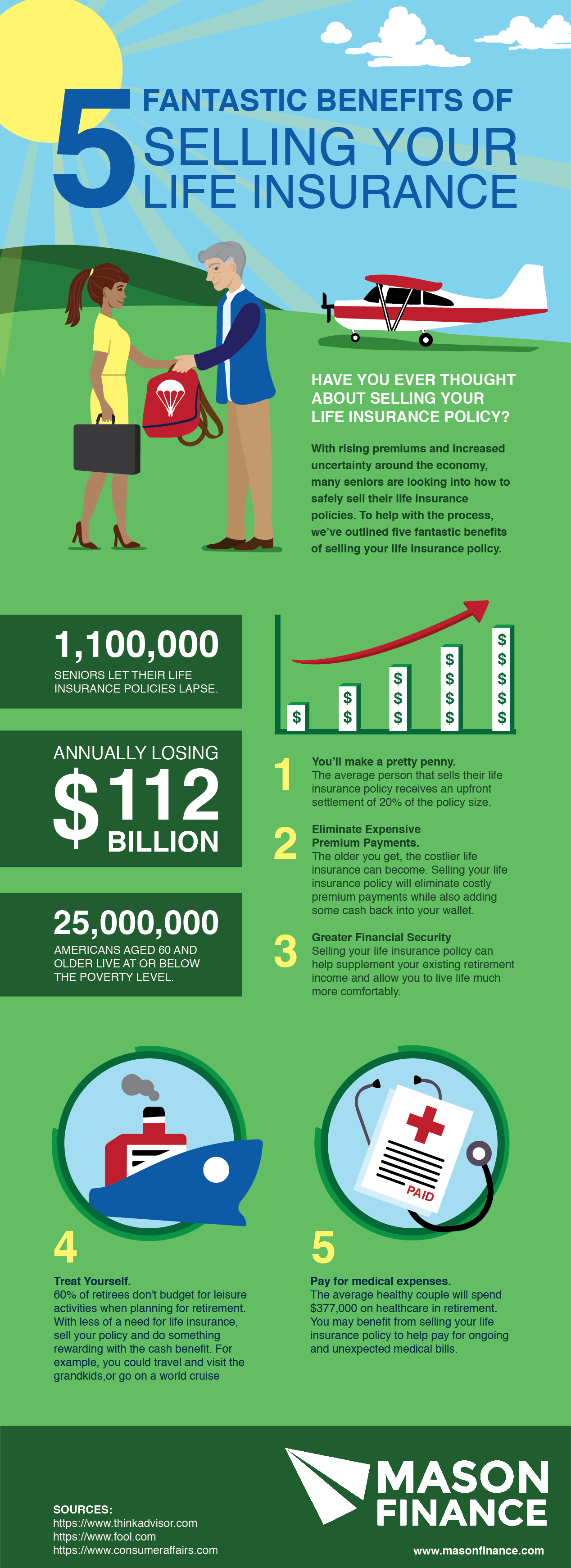

Why Sell Your Life Insurance

At this point, you might be wondering why would you sell your life insurance. Here are some of the most common reasons people choose a life settlement.

- You can no longer afford the premium payments. Premiums often increase as you age and can be difficult to afford on a strict retirement budget. If you are afraid you might lapse on your policy, a life settlement is definitely an option to consider.

- You need the money for other expenses. Medical and long term care costs can be thousands of dollars annually, and selling your life insurance can help to cover these costs.

- You no longer require the coverage. If your dependents do not need protection from the policy anymore, selling your life insurance often makes sense.

- You want more money to enjoy retirement. Sometimes, policyholders just want extra cash to supplement their retirement income, and selling your life insurance can be a great way to achieve this goal.

While life settlements make sense for some people, if you want your beneficiaries to receive the death benefit or you still need the coverage, a life settlement is not a good choice.

Despite the incredible opportunity presented by life settlements, many people allow their policies to lapse because they are simply unaware of the option. Annually, 250,000 policyholders lapse on their payments, missing out on an average of $51,300 each. This money can help cover long term care costs, mortgage payments, home repairs, medical bills, or just allow you to enjoy your retirement with more disposable income, so it is crucial for more people to understand life settlements. For a fast, free estimate check out this life settlement calculator.

Felix Steinmeyer is CEO of Mason Finance Inc. of San Francisco. He is a licensed life insurance settlement provider, member of LISA and received his MS and MBA from Stanford University.

Felix Steinmeyer is CEO of Mason Finance Inc. of San Francisco. He is a licensed life insurance settlement provider, member of LISA and received his MS and MBA from Stanford University.